Serving Layer

REST API + Interactive Dashboard

The batch pipeline writes Parquet outputs once (or on schedule). The FastAPI server is the low-latency serving layer on top: reads outputs, caches DataFrames in memory with a 1-hour TTL, and answers queries in milliseconds.

| Method | Path | Purpose | Latency |

|---|

| GET |

/health |

Liveness check: returns available stores and cache status |

<1 ms |

| GET |

/stores |

Lists all stores with completed pipeline outputs |

<1 ms |

| GET |

/stores/{store}/items |

Lists item IDs, filterable by category or department |

<5 ms |

| GET |

/forecast/{store}/{item_id} |

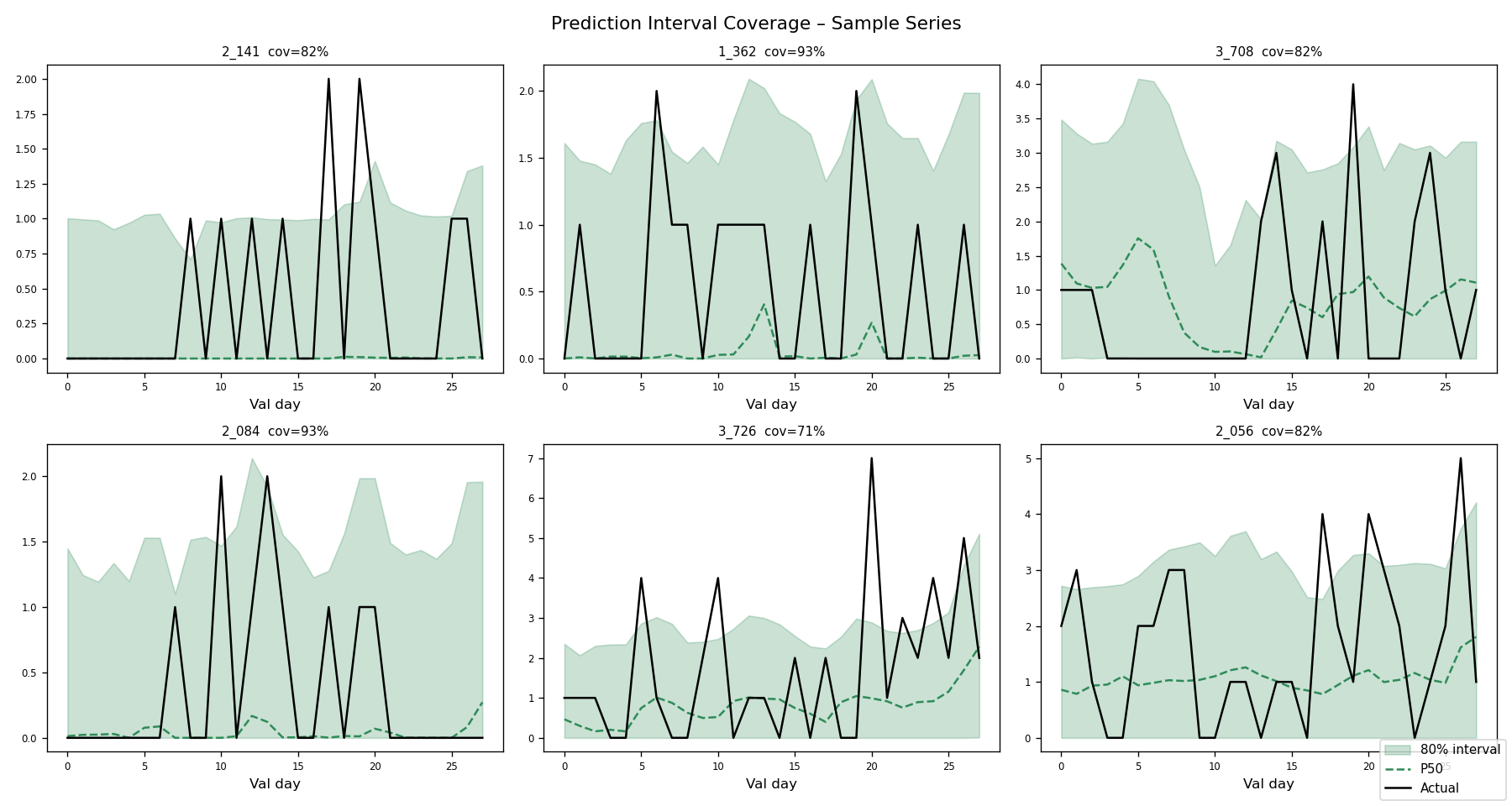

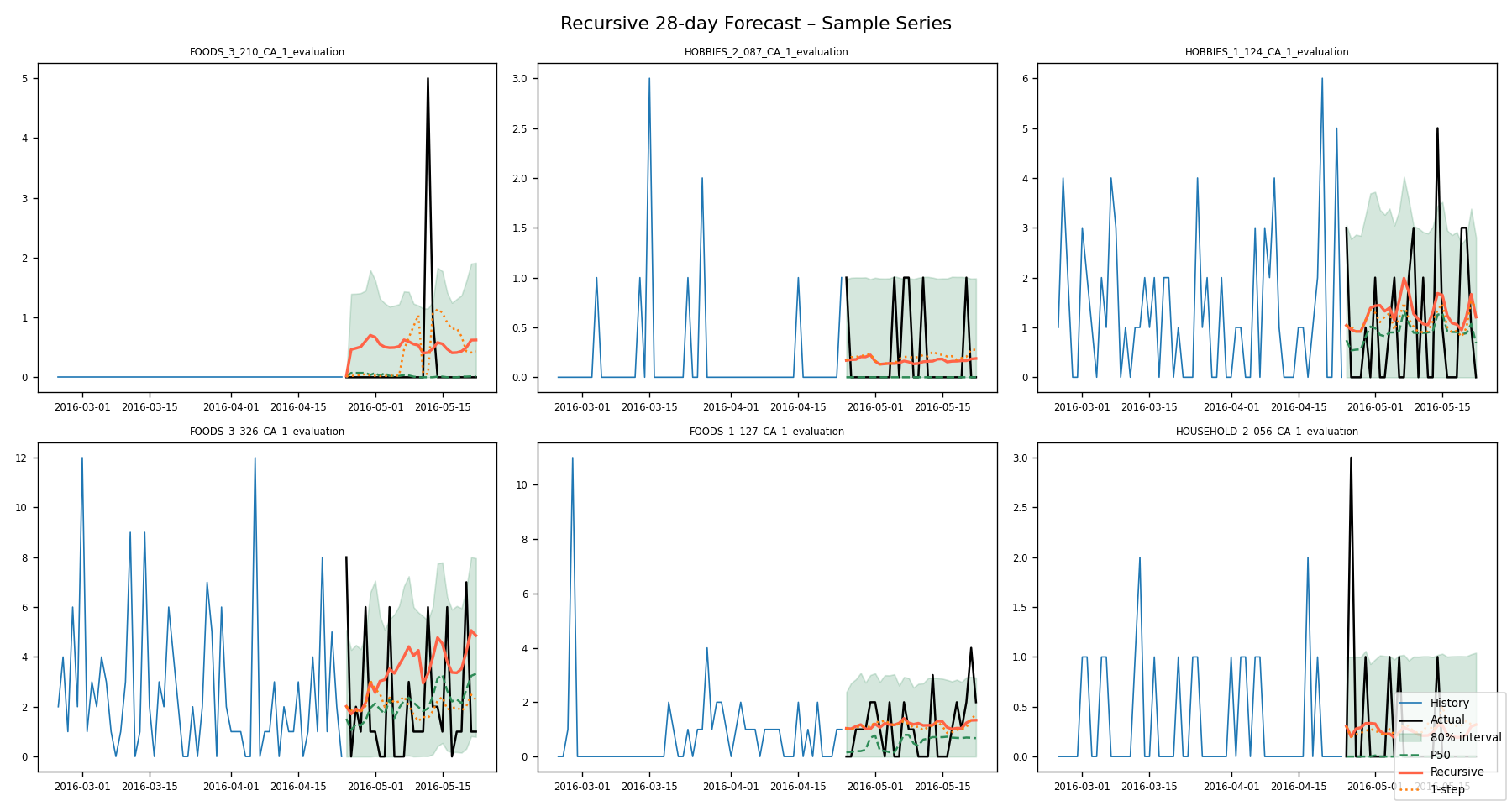

28-day point + quantile forecast (pre-computed from Parquet) |

<5 ms |

| POST |

/inventory |

Live inventory params: any lead time or service level |

<1 ms |

| GET |

/metrics/{store} |

Store-level WRMSSE and walk-forward CV |

<2 ms |

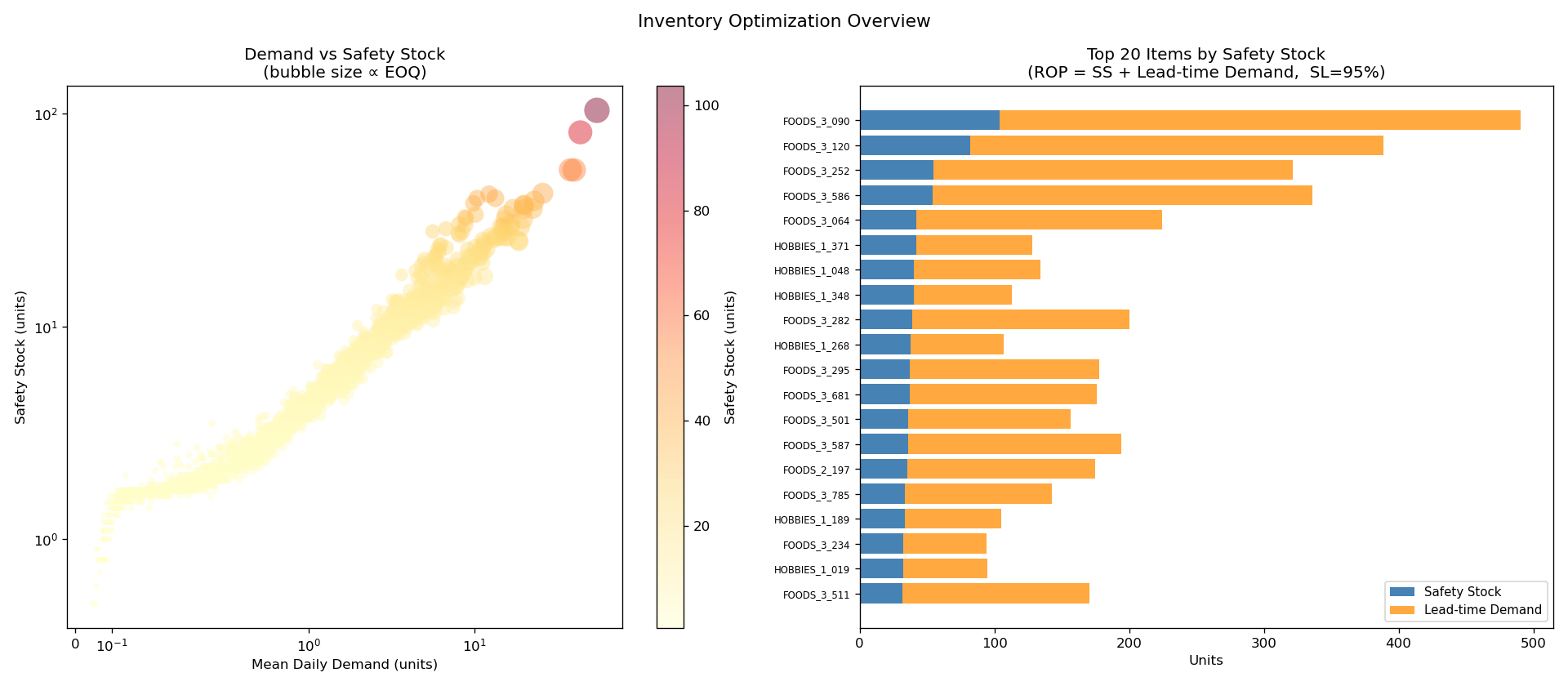

Design note: /forecast reads from Parquet, not from the live model. This means sub-millisecond response times at the cost of freshness (refresh by re-running Phase 5). /inventory computes on-the-fly, letting users query any lead time or service level without re-running Phase 6.

Example: Forecast Response

GET /forecast/CA_1/FOODS_1_001_CA_1_evaluation

{

"store": "CA_1",

"item_id": "FOODS_1_001_CA_1_evaluation",

"n_days": 28,

"forecasts": [

{

"date": "2016-04-25",

"pred_point": 0.7978,

"pred_q10": 0.0,

"pred_q50": 0.9599,

"pred_q90": 2.5654,

"actual_sales": 2.0

},

... 27 more days

]

}

Example: Inventory Response

POST /inventory

{ "store": "CA_1", "item_id": "FOODS_1_001_CA_1_evaluation",

"lead_time": 7, "service_level": 0.95 }

{

"mean_daily_demand": 0.861,

"demand_std_daily": 0.902,

"lead_time_demand": 6.02,

"safety_stock": 3.9, ← hold this much buffer

"reorder_point": 9.9, ← order when stock hits this

"eoq": 396.3, ← order this many units

"days_of_supply_ss": 4.6

}

Tech Stack

Data Processing

pandas, numpy, pyarrow, fastparquet

ML / Forecasting

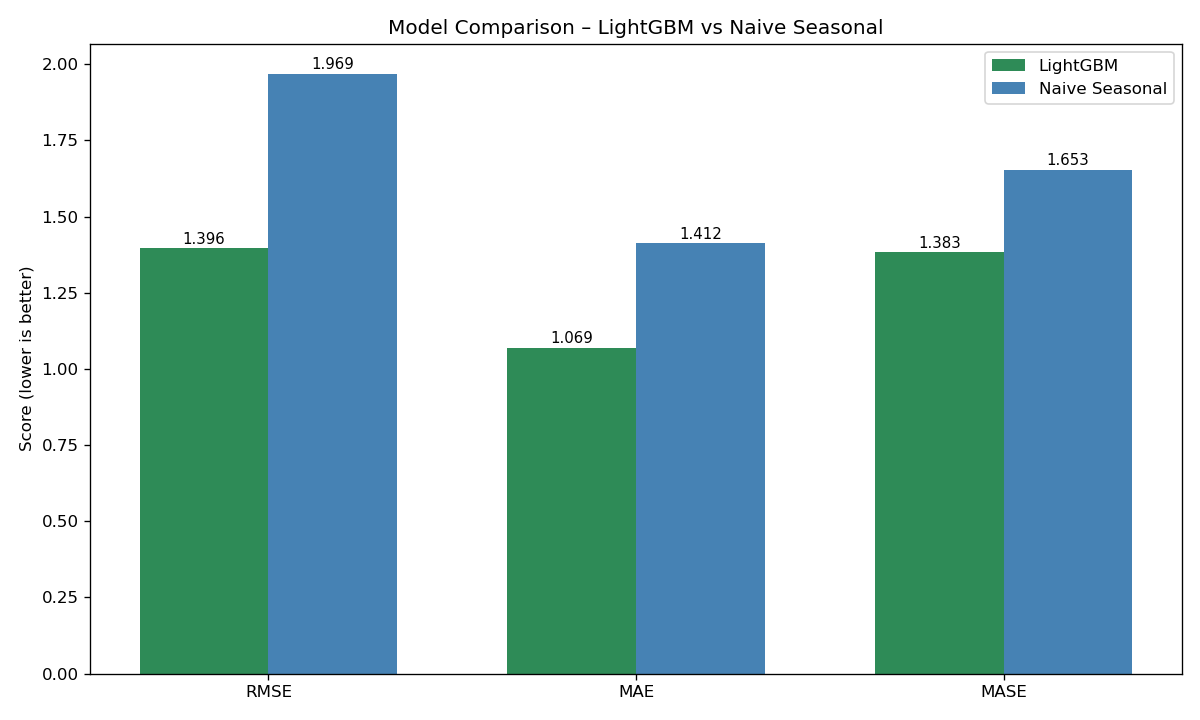

LightGBM, statsmodels (ARIMA), Prophet, scikit-learn

Optimization

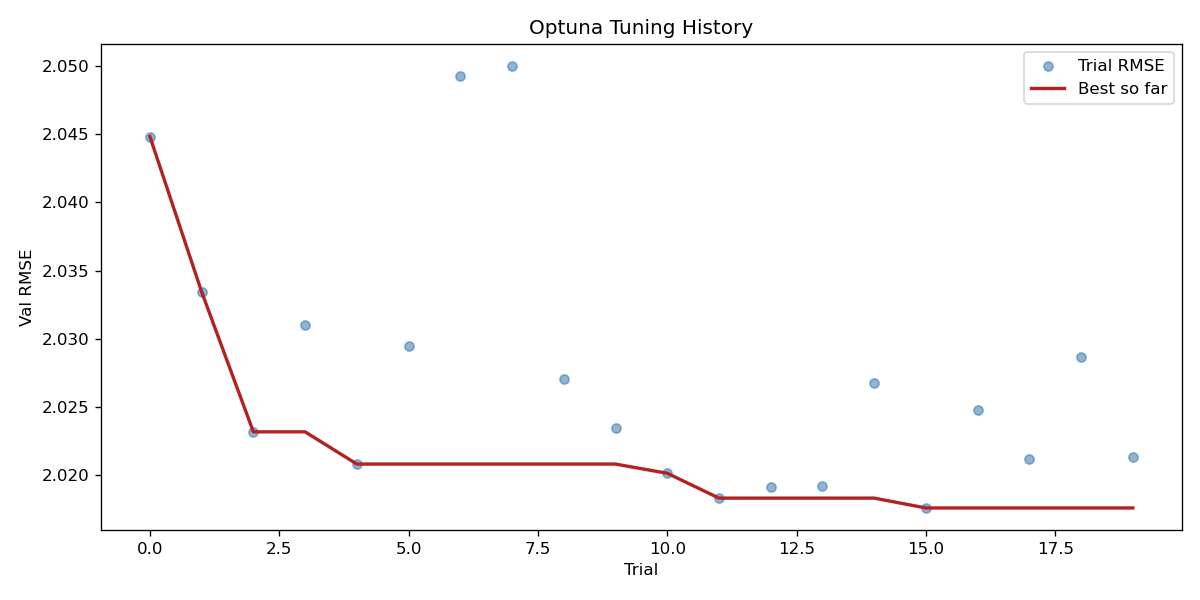

Optuna (TPE sampler), 20-trial Bayesian HPO

Visualization

matplotlib, seaborn, plotly

API / Serving

FastAPI, uvicorn, Pydantic v2, TTL in-process cache

Dashboard

Streamlit (5-tab interactive app with live parameter sliders)